A long-standing challenge in the GST appeals process, relating to mandatory pre-deposit payments, has finally been addressed with the introduction of Form GST DRC-03A, offering relief to taxpayers who were earlier caught in technical and procedural gaps.

The Pre-Deposit Rule in GST Appeals

Under GST law, taxpayers filing a first appeal must pay:

- 100% of admitted tax, and

- A prescribed percentage of disputed tax (typically 10%) as a pre-deposit.

This payment is a prerequisite for filing an appeal before the Appellate Authority under Section 107 of the CGST Act.

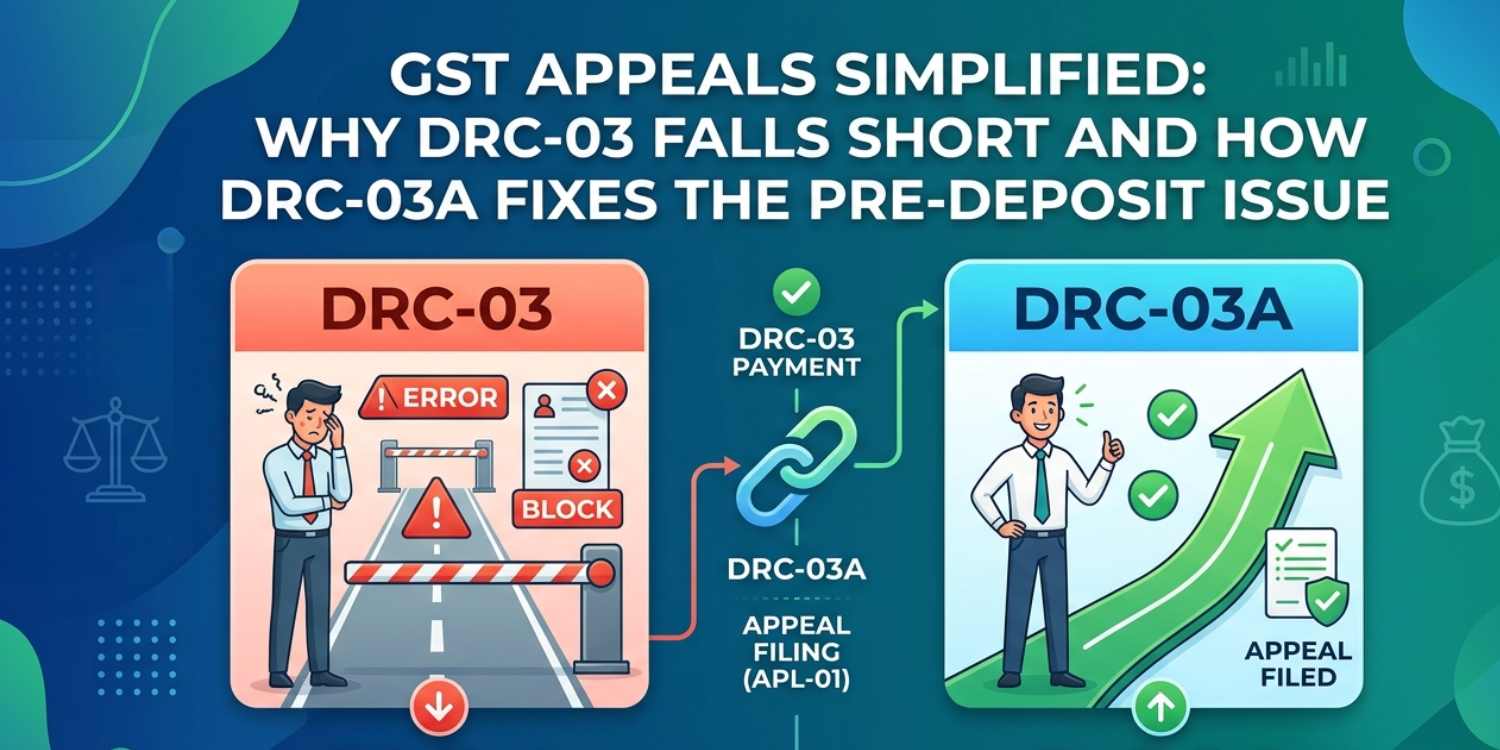

The Problem: Why DRC-03 Was Not Enough

Form GST DRC-03 is primarily designed for voluntary tax payments, such as payments made during audits or investigations.

However, a major issue arose:

- Payments made through DRC-03 were not linked to specific demand orders in the GST system.

- As a result, such payments were not recognised as valid pre-deposits while filing appeals.

- In many cases, taxpayers were forced to pay the same amount again, effectively leading to double payment of GST.

This mismatch created significant litigation and confusion, with courts occasionally intervening in favour of taxpayers facing genuine technical constraints.

The Fix: Introduction of DRC-03A

To resolve this issue, the GST framework introduced Form GST DRC-03A, along with amendments to Rule 142 of the CGST Rules.

Key features include:

- Allows taxpayers to link payments made via DRC-03 to specific demand orders

- Enables such payments to be treated as valid pre-deposits for appeals

- Prevents duplication by adjusting earlier payments against appeal requirements

In essence, DRC-03A acts as a reconciliation mechanism, ensuring that previously paid amounts are not ignored by the system.

Impact on Taxpayers and Litigation

The introduction of DRC-03A is expected to:

- Reduce unnecessary financial burden on taxpayers

- Minimise appeal rejections due to technical non-compliance

- Bring clarity and consistency to GST appeal procedures

Recent updates also indicate that the GST system now recognises such adjustments more effectively, eliminating the earlier issue of duplicate payments during appeal filing.

Conclusion

The shift from DRC-03 to DRC-03A marks a significant procedural correction in India’s GST regime. By addressing a critical gap in the pre-deposit mechanism, the government has streamlined the appeals process and reduced avoidable disputes, making compliance more practical and taxpayer-friendly.