Choosing the right bank account is a crucial step toward effective financial management, ensuring security, convenience, and financial growth. Banks offer a wide range of accounts designed to cater to different needs, whether it’s for individuals seeking a secure place to save, salaried professionals requiring hassle-free transactions, businesses managing high-volume financial operations, or Non-Resident Indians (NRIs) looking to maintain financial ties with India.

Each account type comes with unique features, benefits, and suitability based on financial goals, transaction requirements, and investment preferences. Understanding these options enables individuals and businesses to optimize their banking experience, access essential services, and make informed financial decisions that align with their short-term and long-term objectives. By selecting the right account, customers can not only safeguard their money but also take advantage of value-added services such as digital banking, investment opportunities, and preferential interest rates, ultimately leading to better financial stability and growth.

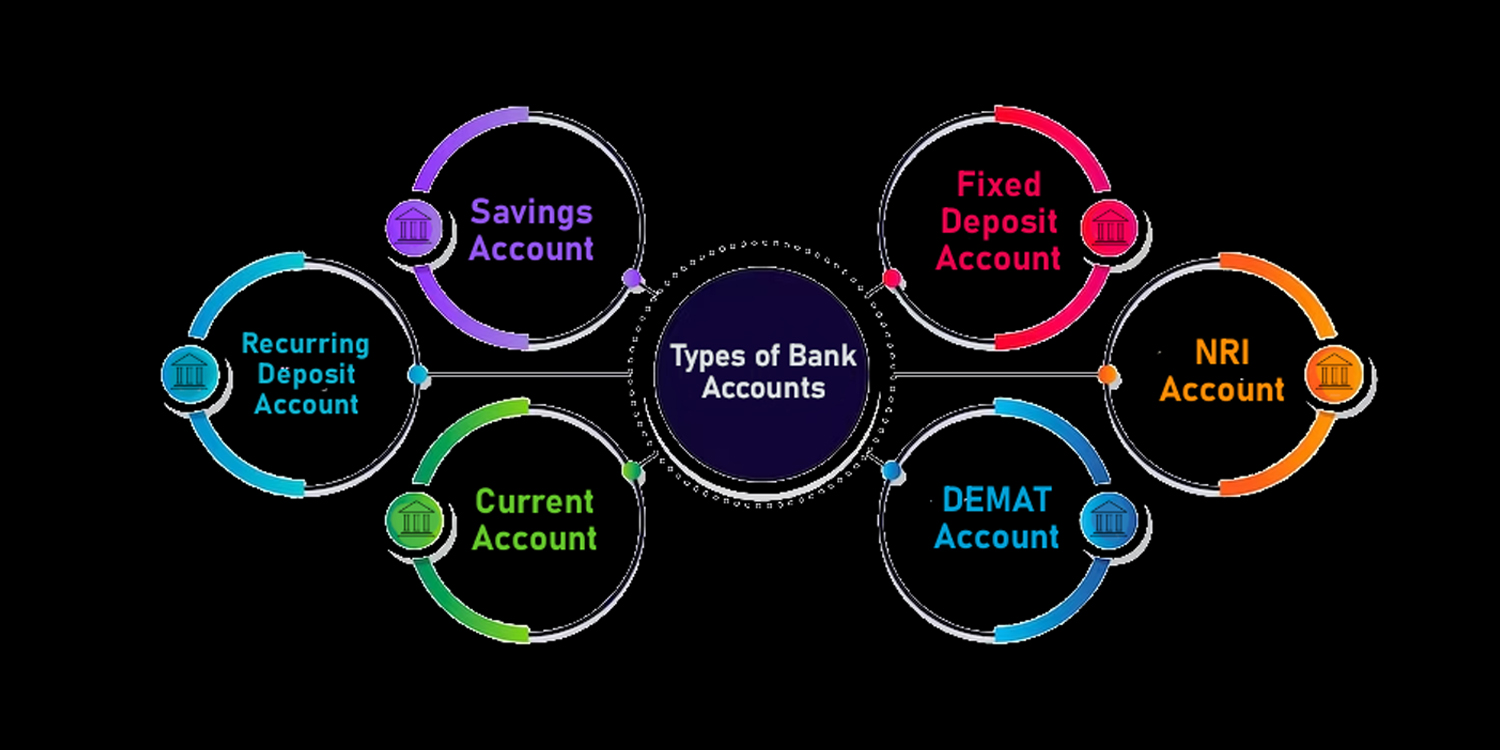

Current Account

A current account is designed for individuals and businesses that conduct frequent transactions. Unlike a savings account, which limits the number of withdrawals per month, a current account allows unlimited transactions, making it ideal for businesses, self-employed professionals, and traders who need seamless cash flow management.

What are the advantages of the current account?

One of the key advantages of a current account is the overdraft facility, which enables account holders to withdraw more than their available balance, offering financial flexibility. However, since it is meant for daily transactions, a current account does not earn interest on deposits. Additionally, most banks require a substantial minimum balance, and failing to maintain it may result in penalties. The account also comes with features such as checkbooks, demand drafts, and online banking services, which are essential for business operations.

Whom is the current account best suited for?

A current account is best suited for businesses, firms, and professionals who require quick and frequent access to their funds.

Savings Account

A savings account is the most commonly used type of bank account, ideal for individuals looking to deposit their money safely while earning interest. It is designed to promote saving habits while providing easy access to funds when needed.

What makes a savings account different?

Unlike current accounts, savings accounts earn interest on deposits, though the interest rates vary across banks. While withdrawals are permitted, they may be subject to monthly limits depending on the bank’s policy. Some savings accounts require a minimum balance, while others, such as zero-balance savings accounts, do not. Additionally, digital banking features, including fund transfers and bill payments, make managing finances more convenient.

Whom is the savings account best suited for?

A savings account is suitable for salaried employees, students, and retirees who want a secure place to store and grow their money.

Salary Account

A salary account is a specialized savings account opened by companies for their employees to facilitate monthly salary deposits. This account typically does not require a minimum balance, making it a cost-effective option for employees.

What are the benefits of a salary account?

One of the major benefits of a salary account is the instant salary credit, ensuring that employees receive their salaries without delays. Banks also provide exclusive perks, such as discounts on loans, credit cards, and other financial products, to salary account holders. However, if an employee leaves the company, the salary account is usually converted into a regular savings account, requiring the account holder to maintain a minimum balance.

Whom is the savings account best suited for?

A salary account is beneficial for employees who want hassle-free salary deposits and additional banking privileges.

Fixed Deposit (FD) Account

A fixed deposit (FD) account is an excellent choice for individuals looking to invest their money securely and earn higher interest rates than a regular savings account. In an FD, a lump sum amount is deposited for a fixed tenure, during which it earns interest at a predetermined rate.

Why should you invest in a fixed deposit account?

Fixed deposits offer significantly higher interest rates compared to savings accounts, and the returns are guaranteed, making them a low-risk investment. The deposit period can range from a few months to several years, with longer tenures typically offering higher interest rates. However, premature withdrawals may attract penalties, so it is advisable to invest only surplus funds that you do not need for immediate expenses.

Whom is the savings account best suited for?

Fixed deposits are best suited for individuals seeking stable and secure investment opportunities with assured returns.

Recurring Deposit (RD) Account

A recurring deposit (RD) account is similar to a fixed deposit but allows individuals to deposit a fixed sum at regular intervals rather than a lump sum. It is ideal for those who want to save consistently over time while earning interest.

What are the advantages of a Recurring Deposit account?

One of the key advantages of an RD is that it encourages disciplined savings, as individuals must deposit a fixed amount every month. The interest rates offered are comparable to fixed deposits, making it a lucrative savings option. RD accounts come with flexible tenures, typically ranging from six months to ten years. However, if a monthly deposit is missed, penalties may apply.

Whom is the RD account best suited for?

RDs are ideal for individuals with a regular income who want to develop a habit of systematic savings while earning decent returns.

DEMAT Account

A DEMAT (Dematerialized) account is essential for anyone who wishes to trade in the stock market. It allows investors to store securities like stocks, bonds, and mutual funds in electronic form, eliminating the need for physical share certificates.

How does a DEMAT account simplify investing?

A DEMAT account provides a secure and convenient way to store financial assets, minimizing the risk of loss or damage. Linked to a trading account, it allows investors to buy and sell shares effortlessly. By digitizing investments and eliminating paperwork, a DEMAT account streamlines portfolio management and ensures seamless transactions.

Whom is the RD account best suited for?

A DEMAT account is ideal for investors looking to grow their wealth through stock market investments.

NRI Accounts

NRI accounts provide a convenient and efficient way for Non-Resident Indians to manage their finances in India while residing abroad. With options tailored for savings, investments, and repatriation, these accounts ensure seamless transactions, tax benefits, and regulatory compliance, making financial management secure and hassle-free for NRIs looking to maintain financial ties with India.

What are the benefits of an NRI account?

NRI accounts offer secure and efficient financial management for overseas Indians. They enable easy repatriation of funds, provide attractive interest rates, and ensure compliance with Indian banking regulations. These accounts also facilitate seamless investments in Indian markets, real estate, and other financial instruments.

Whom is the NRI account best suited for?

NRI accounts are best suited for Indians living abroad who need a reliable way to manage their income in India or send earnings back home while enjoying financial benefits like tax exemptions and repatriation flexibility.

Types of NRI Accounts

Non-Resident External (NRE) Account

An NRE (Non-Resident External) account allows NRIs to deposit their foreign earnings in India. Money is deposited in foreign currency and converted into Indian rupees. One of the main benefits of an NRE account is that both the money deposited and the interest earned can be sent back to a foreign country without any limits. Also, the interest earned is not taxed in India. This account is best for NRIs who want to save their foreign income in India while keeping the option to transfer funds freely. NRE accounts can be opened as savings, current, or fixed deposit accounts, giving flexibility for different financial needs.

Non-Resident Ordinary (NRO) Account

An NRO (Non-Resident Ordinary) account is for NRIs who earn money in India, such as rental income, dividends, or pensions. Unlike the NRE account, money in an NRO account cannot be freely sent abroad. NRIs can transfer up to $1 million per year, but they need to follow tax rules. Also, the interest earned is taxed in India, and a tax of up to 30%is deducted before they receive the interest. However, if India has a tax agreement with an NRI’s home country, they may get tax benefits. The NRO account can also be held jointly with an Indian resident, making it a good option for managing expenses in India.

Foreign Currency Non-Resident (FCNR) Account

An FCNR (Foreign Currency Non-Resident) account is a fixed deposit account where money is kept in a foreign currency, such as USD, GBP, EUR, or other major currencies. Since it is not converted into Indian rupees, it is protected from changes in currency value. This means NRIs do not have to worry about their savings losing value due to rupee depreciation. The interest earned is tax-free in India, and both the deposit and interest can be fully sent abroad. FCNR accounts have a minimum term of one year and a maximum of five years, making them a safe long-term investment.

NRIs can choose the right account based on their needs—whether to transfer foreign earnings, manage income in India, or protect savings from currency changes. Each type of account offers specific benefits to help NRIs handle their finances smoothly while following Indian banking and tax rules.

Benefits of a Bank Account

A bank account is more than just a place to store money—it serves as a gateway to financial security, convenience, and growth. Keeping funds in a bank ensures safety and protection, reducing the risks associated with cash handling while offering fraud protection and insurance coverage on deposits. This guarantees peace of mind, knowing that money is secure and easily accessible.

One of the major advantages of a bank account is easy access to funds. With ATM withdrawals, online banking, mobile apps, and UPI transactions, customers can manage their money anytime, anywhere. Whether making purchases, transferring funds, or paying bills, banking services streamline financial transactions.

Bank accounts also help individuals earn interest on savings, allowing money to grow instead of sitting idle. Savings accounts, fixed deposits, and recurring deposits offer attractive interest rates, encouraging long-term financial discipline. Additionally, structured tools like automatic bill payments and expense tracking promote better financial planning.

For businesses, a bank account is essential for managing transactions and maintaining credibility. A current account enables smooth financial operations, tax compliance, and transparent record-keeping, making it easier to handle payments and receive funds from clients.

Another key advantage is access to credit and investment opportunities. Banks offer loans, overdraft facilities, and investment options, helping customers meet financial goals. Additionally, digital banking services provide a cashless transaction experience, eliminating the dependency on physical money while enhancing security.

In summary, a bank account is a fundamental financial tool that simplifies transactions, promotes disciplined saving, and provides access to loans and investments. Whether for individuals, businesses, or NRIs, it plays a crucial role in ensuring financial stability and growth.

Conclusion:

Bank accounts play a vital role in financial security and management, offering tailored solutions for saving, investing, and daily transactions. They provide a safe place to store money while enabling convenient access through digital banking. Whether for individuals, businesses, or investors, the right bank account helps streamline financial operations, ensuring liquidity, disciplined savings, and long-term wealth creation. Features like interest earnings, automated transactions, and investment integration further enhance financial planning.

Additionally, digital advancements have made banking more accessible, allowing users to manage their finances from anywhere. Choosing the appropriate account based on personal or business needs ensures maximum benefits, from seamless transactions to structured savings and investment opportunities. With various options available, from savings accounts to specialized NRI accounts, banking institutions offer flexible and secure financial solutions. Understanding these choices empowers individuals and businesses to optimize their financial resources, paving the way for a stable and prosperous future.

FAQs:

- Which bank is best for a savings account in India?

The best bank depends on interest rates, fees, and services. Popular choices include SBI, HDFC, ICICI, and Axis Bank. - What is KYC in banking?

KYC (Know Your Customer) is a process where banks verify a customer’s identity using documents like Aadhaar, PAN, and address proof. - How many bank accounts can a person have?

There is no limit, but managing multiple accounts can be complex due to minimum balance requirements and maintenance fees. - How do I know my bank account type?

Check your passbook, net banking portal, or bank statement, or visit your bank branch for account details. - How do I get a bank statement online?

Log in to your bank’s net banking or mobile app, select the account, and download the statement for your preferred period.

Discussion about this post